Your Guide to Tear Trough Treatment in Cape Cod

Considering tear trough treatment? This guide explains fillers, fat transfer, and surgery options at Cape Cod Plastic Surgery to refresh your look.

Dec 26, 2025

Yes, you absolutely can get financing for cosmetic surgery even with bad credit. It’s a common misconception that a low credit score is an automatic "no." The reality is, many modern lenders and specialized financing companies look at your whole financial picture, not just a three-digit number. They're often more interested in your current income and your ability to handle payments now.

Staring at the price tag for a procedure you’ve been dreaming of can feel discouraging, especially if your credit history isn't perfect. But take a breath—it’s far from a hopeless situation. The world of medical financing has evolved, and lenders have become much more sophisticated. They understand that a credit score is just a snapshot in time, and it doesn't always tell the full story of your financial stability today.

This guide is built for people in your exact situation. We'll show you that your ability to manage payments now often matters more than financial mistakes you might have made years ago. There are financing paths designed specifically for this.

A traditional bank might glance at a low FICO score and show you the door. Thankfully, lenders who specialize in the medical and cosmetic fields play by a different set of rules. They've learned to look for signs that you’re a reliable borrower in the here and now.

So, what do they care about?

Your credit score is just one part of your story. Lenders who work in cosmetic surgery financing know this. They often give more weight to your current financial habits and stability than a number from your past.

Now, while getting financing is definitely possible, it's smart to go in with realistic expectations. A lower credit score usually means you'll be offered a higher interest rate. That’s just how lenders balance their risk. The goal isn't simply to get a "yes"—it's to secure a loan with terms you can genuinely afford without adding a new layer of financial stress to your life.

In the following sections, we'll walk you through all the real-world options on the table. We’ll cover everything from medical credit cards and personal loans to the in-house payment plans we sometimes offer. Think of this as your practical guide to navigating the money side of things, so you can move forward with confidence.

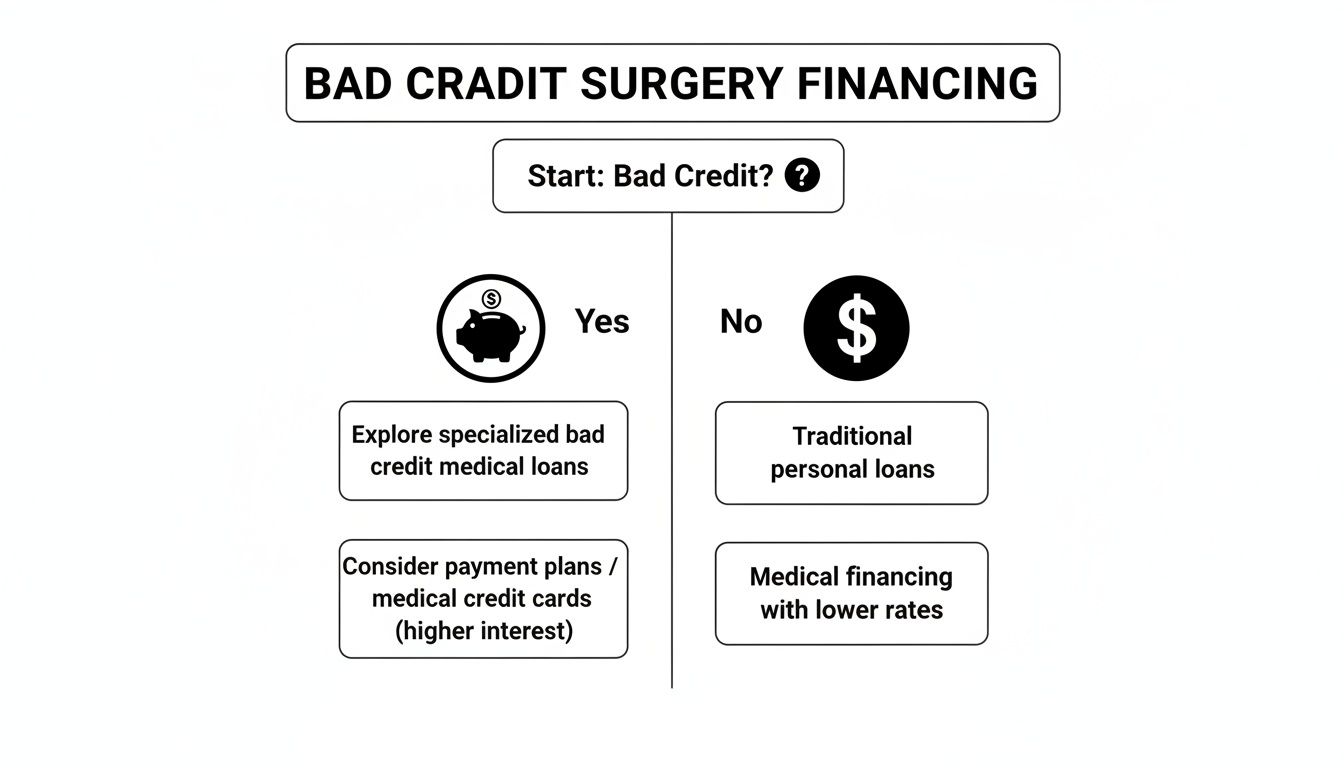

When you’re trying to figure out how to pay for a procedure, you need more than just vague ideas. You need a clear, realistic look at your options for cosmetic surgery financing with bad credit. Let's walk through the most common paths, breaking down the good, the bad, and the fine print for each one.

This quick decision tree can help you visualize which financing routes might open up based on where your credit stands.

The main thing to remember is that "bad credit" doesn't mean "no options." It just means we need to look at a different set of financial tools that are built for your specific situation.

For many people, a medical credit card is the first stop. You’ve probably heard of names like CareCredit or Alphaeon Credit—they’re designed specifically for healthcare costs and most plastic surgery offices accept them.

The biggest appeal? Those promotional financing offers. It’s common to see 0% APR for a limited time, like 6, 12, or even 24 months. This can be an incredible deal, but there’s a big catch: you must pay off the entire balance before that promotional period ends.

Here’s where you need to be careful: deferred interest. If you still owe even a few dollars when the promotional offer expires, the company can go back and charge you interest on the full original amount from day one. With rates often jumping to 26.99% or more, a manageable payment plan can quickly become a huge financial weight.

Another solid path is a personal loan from a lender that specializes in working with people who have less-than-perfect credit. Forget the big banks that might just see a low FICO score and say no. These lenders tend to look at the bigger picture, like your income and recent payment history.

Because they’re taking on more risk, yes, the interest rate will be higher than it would be for someone with a pristine credit report. But what you get in return is stability and predictability.

This kind of straightforward structure means you don't have to worry about a surprise deferred interest bomb. It’s a much more transparent way to finance your procedure.

With several paths to consider, it can be tough to know which one fits your situation best. This table breaks down the key features of the most common financing methods to help you compare them at a glance.

Ultimately, the right choice depends on your financial discipline, your comfort with different types of risk, and the specific terms you're offered.

Some practices, like ours here at Cape Cod Plastic Surgery, offer our own in-house payment plans or have close relationships with specific lenders. This can be one of the most flexible options out there. Since we already have a direct relationship with you as a patient, we can often create a more personalized plan.

In-house financing can sometimes move past the strict credit score algorithms that big lenders use. The focus is more on finding a payment schedule that works for everyone. It’s always a good idea to ask about this during your consultation.

These plans might involve making several payments directly to our office in the months before your surgery. You can find out more about the different ways to approach this by reading through our detailed guide on plastic surgery financing options.

"Buy Now, Pay Later" isn't just for online shopping anymore. Services like Cherry and PatientFi are making a big splash in the medical world. Their approval process is often much faster and simpler than a traditional loan, and many use a soft credit check for the initial application, which won't ding your credit score.

The need for these options is obvious. In 2021 alone, more than 1.56 million plastic surgeries were performed in the U.S., highlighting a massive demand for accessible payment solutions. Recognizing this, some platforms have emerged with approval rates as high as 95%, even for applicants with challenging credit histories.

If you're dealing with a difficult financial past, looking into strategies for getting out of debt with bad credit can be an empowering first step. Getting a handle on existing debts will only make your financial foundation stronger as you prepare to take on a new payment plan.

Getting approved for financing with a less-than-perfect credit score isn't about crossing your fingers and hoping for the best. It’s about being strategic. You can actively build a stronger case for yourself by showing lenders a complete picture of your financial health—one that goes beyond just a three-digit score.

Think of it as presenting evidence. You're aiming to prove your stability and reliability, even if your past credit history has some bumps. By gathering the right documents, making smart financial moves, and sometimes leaning on your support system, you can significantly tip the odds of approval in your favor.

When your credit history is shaky, lenders immediately look for other signs of reliability. Your income and employment history become the most powerful signals you can send.

Before you even start an application, get your financial paperwork organized. Having everything ready not only speeds things up but also shows you're serious and on top of your finances. This simple preparation can make a surprisingly big difference.

Get these key documents together:

This collection of documents paints a much clearer picture of your ability to handle monthly payments. For many lenders who work with bad credit, this proof of stable income is often more compelling than a past financial mistake. Reducing existing liabilities is another smart move; learning how to negotiate credit card debt can improve your overall financial standing.

Want to instantly make your application more attractive? Offer a down payment. Putting some of your own money down reduces the total amount you need to borrow, which directly lowers the lender's risk.

For them, it’s a clear sign of your commitment and ability to manage your money. In my experience, a larger down payment often unlocks better loan terms. Lenders might offer a lower interest rate or a more flexible repayment plan when they see you have more skin in the game. It shows you're a partner in this, not just a borrower.

A down payment of 20% or more can completely change a lender's perception. It signals that you are financially invested and less likely to default, making them far more comfortable with approving your loan.

Even if you can't manage 20%, any amount helps. It proves you have savings and aren't relying entirely on borrowed funds—a major green flag for any lender.

If your own credit and income just aren't strong enough to get an approval, a co-signer with good credit can be a game-changer. A co-signer—usually a trusted family member or close friend—agrees to be legally on the hook for the loan if you can't make the payments.

Their strong credit history acts as a safety net for the lender, often making an approval possible when it otherwise wouldn't be.

This is a huge ask, so don't take it lightly. It’s a serious financial commitment for your co-signer. The loan will show up on their credit report, and any missed payments will damage their score right along with yours.

Before asking someone, make sure you both understand:

A co-signer can make the impossible possible, but that path is built on a foundation of trust and a crystal-clear understanding of the shared responsibility.

If traditional loans and medical credit cards just aren't a good fit, don't throw in the towel. Getting cosmetic surgery financing with bad credit often means you just have to think a little differently and look beyond the most obvious routes. There are actually several creative strategies you can use, and many of them put you in much better financial control.

These approaches are about more than just finding the cash—they're about building smarter financial habits that serve you long after your procedure. Let's dig into some of these less common, but highly effective, ways to make your surgery a reality.

Honestly, the most empowering way to pay for your surgery is with your own money. It takes patience, I know, but saving up means you avoid interest payments, stressful loan applications, and the risk of hurting your credit score even more. It’s the one guaranteed debt-free path.

Think of it this way: a dedicated savings plan turns a big, scary number into a series of small, manageable steps.

Here’s how to do it right:

A realistic budget is everything. Take one month and track every single dollar to see where your money is really going. You might be surprised to find "leaks" in your budget—like daily coffees or subscriptions you forgot about—that can be redirected straight to your surgery fund.

Platforms like LendingClub or Prosper have shaken up the old-school lending world. They are essentially online marketplaces that connect people who need to borrow money directly with individual investors who are willing to fund them. For someone with a rocky credit history, this can be a game-changer.

Why? Because investors on these sites often look beyond a simple FICO score. They consider your personal story, your income stability, and the reason you need the loan. A well-written, honest explanation can sometimes make all the difference. While approval isn't a sure thing and the rates can still be high for lower credit scores, it’s definitely an avenue worth exploring.

It's clear that patients need more accessible financing options. In fact, nearly 70% of patients now say financing is essential for moving forward with cosmetic procedures. This demand has pushed clinics to partner with more flexible third-party platforms. In the U.S., where a FICO score below 579 often means an automatic "no" from traditional banks, these alternative solutions are becoming more important than ever.

Do you own an asset like a car that's paid off or has a good amount of equity? A secured loan might be on the table for you. Unlike a personal loan that’s based only on your credit score, a secured loan is backed by your asset as collateral. This makes you a much less risky borrower in the lender's eyes.

The benefits can be significant:

But you have to be extremely careful here. This path comes with a major risk: if you fail to make your payments, the lender can and will seize your asset to cover their loss. Only consider this if you are absolutely confident in your ability to repay the loan without fail.

No matter which road you decide to take, the first step is always understanding the full cost. Here at Cape Cod Plastic Surgery, we believe in being completely transparent about pricing. Our team can give you a clear picture of the investment required, which helps you build a solid financial plan. Take a look at our general payment plans information to get a better idea of how we work with patients to make their goals achievable.

Getting the green light for cosmetic surgery financing with bad credit is definitely possible, but it's crucial to go into it with your eyes wide open. High-interest loans come with some serious risks that can quickly turn a manageable payment into a heavy financial weight if you're not careful. This isn't to scare you off, but to help you read the fine print and make a choice you feel good about long-term.

It's true that the world of cosmetic financing is booming. Projections show the market soaring from $35.80 billion in 2024 to over $60.78 billion by 2032. This growth means more options are popping up, even for those with less-than-perfect credit. But more options also mean you have to be extra sharp about the terms you agree to. You can dig deeper into the growth and risks in the cosmetic financing market to see the full picture.

The Annual Percentage Rate (APR) isn't just the interest; it’s the total cost of borrowing money, fees and all. When your credit score is on the lower side, lenders see you as a bigger risk, so they charge a higher APR to protect themselves. The difference this makes over the life of a loan can be genuinely shocking.

Let’s run the numbers on a $10,000 procedure.

That high APR almost doubles the price of your surgery. It’s a perfect illustration of why you have to carefully weigh the long-term cost against the immediate desire to have the procedure done now.

The total interest you pay is the hidden price tag of financing with bad credit. Before you sign anything, always plug the numbers into a loan calculator to see the full cost. A slightly lower monthly payment spread over a longer term can easily conceal thousands of dollars in extra interest.

You've probably seen the ads for medical credit cards like CareCredit, flashing a tempting "0% interest" promotional period. This can be a fantastic tool if—and this is a big if—you pay off every single penny before that period ends.

Here’s the catch: it's not a true 0% APR. It’s deferred interest. This means if you have even $1 left on your balance the day the promotion expires, the lender can legally reach back to day one and charge you interest on the entire original amount. Suddenly, a rate of 26.99% or more is applied retroactively, and your balance can explode overnight.

This one clause, often buried in the fine print, can turn a smart financial plan into a disaster. If you go this route, you need an ironclad strategy to pay it off in full and on time.

The real irony of taking on a high-risk loan is that it can trap you in a worse financial position. Just one missed or late payment will get reported to the credit bureaus, knocking your already low score down even more.

This kicks off a vicious cycle. A lower credit score makes it harder and more expensive to borrow for anything else in the future, whether it's a car, a home, or another personal need. That’s why you have to be absolutely certain you can handle the monthly payments without fail before committing. Your future financial health is riding on it.

You've done the hard part—the research. You now know that having less-than-perfect credit doesn't automatically close the door on cosmetic surgery. With a better understanding of everything from in-house plans to specialized medical lenders, you can confidently move forward.

This next phase is all about turning that knowledge into a personalized action plan. It's about having a real conversation and seeing what's truly possible for you.

The very first step is a simple, confidential chat with Dr. Marc Fater and our team. Think of this as a no-pressure meeting to talk about your goals, ask all your questions, and get a clear picture of what we can achieve together.

Our focus is entirely on you—your vision, your health, and your comfort. We'll map out a surgical plan that's tailored specifically to your goals, building a foundation of trust right from the start.

Your credit score doesn't define you, and it shouldn't stand in the way of your goals. Our team provides a supportive, non-judgmental space focused on finding a viable path forward, not dwelling on past financial hurdles.

This initial discussion is the cornerstone of your entire journey. It’s where you get to know us, and we get to understand what you're hoping for.

A brilliant surgical result needs a smart financial plan to make it happen. Our patient care coordinators are experts in this area and will be your personal guides. They’ll sit down with you to create a clear, manageable plan that works for your budget.

Here’s how we’ll support you:

This hands-on approach ensures you feel informed and in control of your investment in yourself.

Ready to get started? Here’s a simple checklist to prepare for your visit with us at Cape Cod Plastic Surgery.

Deciding to have cosmetic surgery is a major step. Here at Cape Cod Plastic Surgery, we’re dedicated to making you feel supported, respected, and empowered every step of the way. It all begins with that first call.

Considering tear trough treatment? This guide explains fillers, fat transfer, and surgery options at Cape Cod Plastic Surgery to refresh your look.

July 1, 2026

Transforming Your Body and Improving Wellness After Massive Weight Loss

June 30, 2026

Understand the full gynecomastia surgery cost in 2026. This guide breaks down fees, factors, insurance, and financing options to help you plan your budget.

Cape Cod Plastic Surgery offers expert cosmetic and reconstructive procedures in a safe, accredited setting. Led by Dr. Marc Fater, we combine advanced techniques with personalized care to help you look and feel your best.

Monday: 9:00 AM – 5:00 PM

Tuesday: 9:00 AM – 5:00 PM

Wednesday: 9:00 AM – 5:00 PM

Thursday: 9:00 AM – 5:00 PM

Friday: 9:00 AM – 5:00 PM