Skin Tightening After Liposuction: Options & Recovery

Considering skin tightening after liposuction? Explore recovery, influencing factors, and effective treatment options, from non-invasive to surgical.

Nov 17, 2025

So, you're wondering if your insurance will pay for surgery to fix a deviated septum. The short answer is yes, but with a big catch: it has to be considered medically necessary.

If the surgery is just to change the look of your nose, insurance companies will almost certainly turn you down. The entire game is about proving the procedure fixes a real, functional problem with your breathing, not just something you don't like in the mirror.

When it comes to getting approval, insurance providers have one main question: are we fixing a health problem or are we paying for a cosmetic upgrade? They draw a very clear line in the sand between function and form.

This is where understanding the two common procedures is crucial. A septoplasty is the surgery to straighten the septum and improve airflow—that's the functional part. A rhinoplasty, often called a "nose job," is usually done to change the nose's outward shape, which is almost always considered cosmetic.

To make it crystal clear, let's break down the core differences between these two surgeries and why one typically gets a green light from insurers while the other doesn't.

Think of it this way: a septoplasty fixes the engine, while a rhinoplasty is like getting a new paint job. Your health insurance is there to make sure the engine runs smoothly.

Your insurance provider is going to want hard evidence that your surgery is essential for your health. This means your doctor will need to document everything—from chronic stuffy noses and recurring sinus infections to breathing problems that genuinely mess with your daily life.

A major analysis of 67 insurance companies found that 55% covered septoplasty, but almost always with preauthorization. The top two requirements for getting that approval were documented nasal obstruction (49%) and clear proof of the deviated septum itself (46%).

Don't worry, we're going to walk you through exactly how to build a rock-solid case for medical necessity and gather all the right paperwork to get the coverage you deserve.

To really get why insurance would pay for a septoplasty, you have to understand the problem it’s fixing. The easiest way to think about your nasal septum is as the central wall dividing your nose into two hallways. When that wall is straight, air moves through both passages easily.

But when that wall is crooked, or “deviated,” it’s like someone shoved a big piece of furniture into one of the hallways. It creates a serious bottleneck. This isn't some rare condition, either. Global studies suggest that a deviated septum might affect as many as 74.5% of people in some populations. You can dig into the numbers yourself with this market research on deviated septums.

For a lot of people, a slightly off-center septum is no big deal. For many others, though, it kicks off a chain reaction of chronic problems that are way more serious than a stuffy nose. This is where the issue crosses the line from a minor annoyance to a legitimate medical necessity.

The constant nasal blockage from a deviated septum isn't just about feeling congested. It can wreck your quality of life, causing problems that basic treatments like nasal sprays or allergy pills just can't touch. And that’s exactly the kind of evidence an insurer is looking for.

When does it become a clear-cut medical need? When you're dealing with symptoms like these:

When these issues become a daily grind—interfering with your sleep, your work, and your general well-being—your surgeon can build a powerful case that surgery isn't just a choice. It's a necessary step to get your body functioning properly again. This well-documented history is the cornerstone of a successful insurance claim.

When your doctor talks about a procedure being "medically necessary," it sounds straightforward. But for an insurance company, that phrase isn't a general suggestion—it’s a very specific, technical definition with a strict checklist. Getting them to answer "yes" to "does insurance cover deviated septum surgery?" is all about proving your case meets their rigid criteria.

Ultimately, it’s less about how much discomfort you're in and more about the documented functional impairment you're experiencing. Think of it as building a legal case. Your symptoms are your claim, but without concrete evidence, the case won't stand up in the insurer's "court." They need a clear paper trail showing that your deviated septum is a genuine medical problem, not just a minor inconvenience or a cosmetic issue.

To get your septoplasty approved, your surgeon has to build a portfolio of proof on your behalf. This isn't just a formality; it's the foundation of the entire preauthorization process. Knowing what they need helps you understand why every doctor's visit and every attempted treatment is a crucial piece of the puzzle. The level of detail required is significant, much like the extensive medical proof required for disability claims.

Here’s what your medical file absolutely must include:

But even with all of that, one piece of evidence trumps all others: proof that you’ve already tried less invasive treatments and they haven't worked.

Insurers almost always require a documented history of failed conservative treatments. This means your medical records must show you've consistently tried things like nasal corticosteroid sprays, antihistamines, or decongestants for at least 3 to 6 months with no meaningful improvement.

This history proves that surgery isn't your first choice, but your last resort. It shows the insurer that you and your doctor have been diligent, making the procedure a true medical necessity. This distinction is critical for separating functional procedures from elective ones, a concept we dig into when comparing reconstructive surgery vs. cosmetic surgery.

Without that documented proof of failed treatments, a denial is almost guaranteed.

Navigating the preauthorization process for surgery can feel like a maze. The good news? You don't have to go it alone. Think of it as a team effort between you and your surgeon's office.

Your job is to clearly communicate your symptoms and history. Their job is to take that information, bundle it with the medical evidence, and present a rock-solid case to your insurance provider. This teamwork is what gets a septoplasty approved as a medical necessity.

The whole process kicks off the moment your surgeon recommends the procedure. From there, their staff will gather everything needed for the preauthorization request: your medical records, photos or scans from your exam, and a history of all the treatments you've tried that didn't work.

Once that packet is sent, a medical reviewer at your insurance company takes over. They're essentially a gatekeeper, and their job is to check your case against a specific list of criteria for coverage. They need to see clear proof that your deviated septum is causing significant issues and that you've exhausted other options.

This review can take anywhere from a few days to a couple of weeks, so a little patience is key.

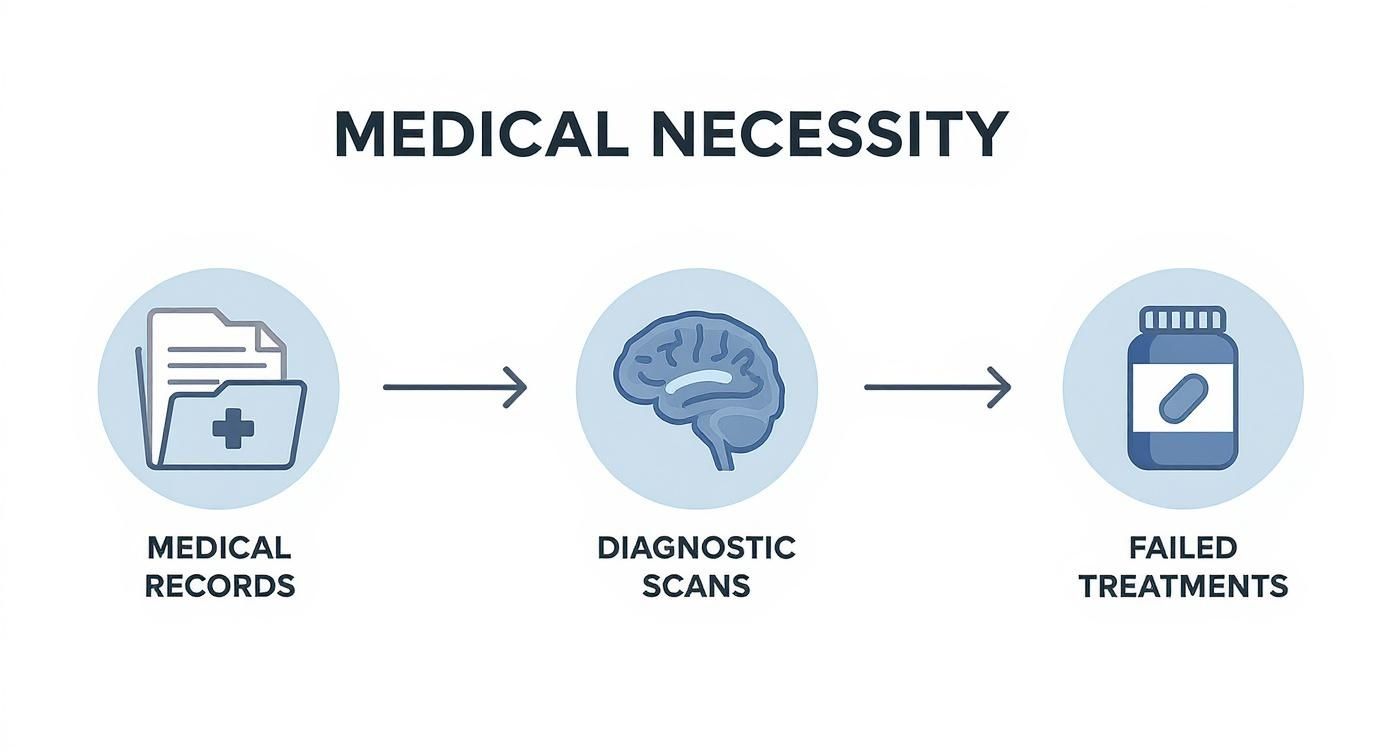

This infographic breaks down the three core pillars of evidence your surgeon will use to build your case.

As you can see, it's not just one thing. It's the combination of documented symptoms, diagnostic proof, and a clear record of failed conservative treatments that gets the green light.

After the review, you'll get a decision. It typically falls into one of three buckets:

Pro Tip: Ask your surgeon's office for a copy of the entire preauthorization packet they send to the insurance company. Having your own records keeps you in the loop and gives you all the documents you'll need if you have to file an appeal. It’s a simple step that can save you a lot of headaches later on.

So, you've gotten the green light from your insurance company for deviated septum surgery. That's great news! But it's crucial to understand that "covered" rarely means "free." You'll still have some skin in the game, and figuring out those costs ahead of time is the best way to avoid any nasty financial surprises.

Your final bill is a direct reflection of your specific insurance plan's design. To get a handle on what you'll actually pay, you need to be familiar with three key terms that pop up in every policy.

Let’s quickly break down the vocabulary your insurance company uses. These three concepts work together to determine your share of the cost.

Putting it all together can be confusing, so let's walk through an example. Seeing the numbers in action makes it much clearer.

The table below shows a possible scenario for a septoplasty to help you visualize how these different cost components interact.

| Example Breakdown of Surgery Costs with Insurance |

| :--- | :--- | :--- | :--- |

| Cost Component | Total Billed Amount | Insurance Pays | Patient Pays |

| Total Procedure Cost | $8,000 | - | - |

| Patient's Deductible | - | $0 | $1,500 |

| Remaining Balance | $6,500 | - | - |

| Coinsurance Split (80/20) | - | $5,200 | $1,300 |

| Total Out-of-Pocket | | $5,200 | $2,800 |

In this case, with a $1,500 deductible and 20% coinsurance, your total responsibility for an $8,000 procedure would be $2,800.

Remember, the final bill often has a few moving parts. You might receive separate invoices for things like the anesthesiologist, the hospital or surgery center's facility fees, and any medications you need after the procedure. Always ask your surgeon’s office for a detailed cost estimate so you can plan accordingly.

While there are upfront costs, research has shown that surgery is often a smart long-term investment. One study highlighted the significant economic benefits of septoplasty on Wiley Online Library, noting that it can save thousands over time by reducing other healthcare needs and lost work days. If you're looking for ways to manage the initial expense, our guide on how to finance cosmetic surgery offers some excellent strategies and payment options.

Getting a denial letter from your insurance company feels like hitting a brick wall. But it’s almost never the final word. Don't panic.

Often, a denial isn't a flat-out rejection of your need for surgery. It's more likely a problem with the paperwork—think of it as a request for more information rather than a permanent "no." With a calm, organized approach, you can often get that decision reversed.

Most denials for septoplasty boil down to surprisingly simple issues. We often see things like missing medical records, a small clerical error, or a submission that just didn't paint a clear enough picture of why the surgery is medically necessary.

The first step is figuring out exactly what went wrong. For a deep dive into this, it's helpful for understanding claim refusal and appeals in general. Your denial letter is your roadmap; it will state the specific reason for their decision.

Once you know why they said no, you and your surgeon's office can work together to build a stronger case. Your doctor's team is your biggest ally here—they do this all the time.

Here’s how to tackle the appeals process, step-by-step:

Remember, you have the right to appeal. The first denial is just the start of a conversation. If the insurer's internal appeal doesn't work, you can often request an external review from an independent third party. Don’t let that first "no" stop you.

When you start digging into insurance coverage for septoplasty, a lot of specific questions pop up. Let's walk through some of the most common ones so you can feel more prepared for the process.

Absolutely, and it's quite common. But here's the crucial part: your insurance will only pay for the septoplasty, which is the medically necessary procedure to fix your breathing.

Your surgeon will need to create a very detailed cost breakdown that separates the functional (septoplasty) part from the cosmetic (rhinoplasty) part. You will be responsible for 100% of the costs associated with the rhinoplasty, as that's considered purely elective.

This is a big one. Most insurance companies want to see that you’ve given conservative treatments a fair shot before they’ll agree to pay for surgery.

Typically, they require a documented history of trying things like nasal corticosteroid sprays and antihistamines for at least 3 to 6 months. Your medical records need to clearly show that these options didn't provide enough relief. Without that paper trail, getting approval for surgery is nearly impossible.

What about Medicare? Medicare follows the same logic as private insurers. It will typically cover a septoplasty if it's proven medically necessary to improve breathing, but you'll still need all the proper documentation and preauthorization.

Once your surgery is done, a smooth recovery is key. Knowing what to watch for, like the signs of infection after septoplasty, is an important part of your aftercare.

At Cape Cod Plastic Surgery, we help our patients navigate every step, from dealing with insurance preauthorization to providing dedicated post-operative care. Schedule your consultation with us today.

Considering skin tightening after liposuction? Explore recovery, influencing factors, and effective treatment options, from non-invasive to surgical.

July 8, 2026

The Gold Standard in Plastic Surgery: Why Board Certification Matters

July 7, 2026

Our 2026 guide explains precisely how does botox work. Discover its science, procedure, benefits, and risks in simple terms to see if it's for you.

Cape Cod Plastic Surgery offers expert cosmetic and reconstructive procedures in a safe, accredited setting. Led by Dr. Marc Fater, we combine advanced techniques with personalized care to help you look and feel your best.

Monday: 9:00 AM – 5:00 PM

Tuesday: 9:00 AM – 5:00 PM

Wednesday: 9:00 AM – 5:00 PM

Thursday: 9:00 AM – 5:00 PM

Friday: 9:00 AM – 5:00 PM