How Does Botox Work: Your 2026 Guide

Our 2026 guide explains precisely how does botox work. Discover its science, procedure, benefits, and risks in simple terms to see if it's for you.

Nov 16, 2025

When you decide you're ready to invest in yourself with a cosmetic procedure, the next big question is always, "How am I going to pay for this?"It's the first real, practical step on your journey. Most people navigate this by looking into personal loans, specialized medical credit cards, or the in-house payment plans that many surgeons now offer. Getting a feel for how each of these works is the key to finding a comfortable fit for your budget.

It’s completely normal to feel a mix of excitement about the procedure and a little bit of anxiety about the cost. Thankfully, the days of needing the full amount in cash upfront are largely behind us. The real goal is to find a financing method that makes sense for your financial situation, giving you a clear and manageable way to pay over time.

This financial flexibility is a big reason why the industry has grown so much. The global cosmetic surgery market hit around $82.5 billion in 2023, and it's on track to nearly double by 2033. Here in the U.S., we've seen a 54% jump in the number of procedures performed each year since 2000, and accessible financing is a huge part of that story. You can dive deeper into these plastic surgery trends on 22plasticsurgery.com.

As you start exploring how to finance your surgery, you'll quickly find there are a few common roads to take. Each has its own set of pros and cons, and knowing the difference is what will help you make a smart, informed decision.

Here are the heavy hitters:

Choosing the right financing isn't just about getting a "yes." It's about finding a plan with terms that won't add stress to your life while you're supposed to be recovering and enjoying your results. Your financial well-being is every bit as important as your physical outcome.

To help you see the differences more clearly, here’s a quick breakdown of how these options stack up.

This table offers a quick comparison of the most common financing methods for cosmetic procedures, highlighting key features to consider.

Ultimately, this comparison is a starting point. The best choice always comes down to what works for you.

The "best" financing option is completely personal. If you're planning a non-invasive treatment, a medical credit card with a six-month 0% APR period might be perfect. On the other hand, if you're preparing for a more significant surgery like a mommy makeover, the stability and often lower fixed rates of a personal loan might be a much better fit.

Your credit score will play a big role, as will your income and just how comfortable you are with taking on a new payment. The goal is to walk into your procedure feeling confident not just in your surgeon, but in the financial plan you've put in place. Take your time, compare the rates and terms, and choose the path that empowers you to make this investment in yourself wisely.

When you’re looking for a straightforward, predictable way to pay for your procedure, a personal loan is often the clearest path. You get the full amount for your surgery upfront in one lump sum, and then you pay it back in fixed monthly installments. This approach eliminates any financial guesswork, which is why it’s such a go-to option for many of our patients.

But before you even start looking at loan offers, the real first step is taking a look at your own financial health. That starts with your credit score. Lenders see this three-digit number as a quick indicator of how reliably you’ve managed credit in the past.

A strong credit score can unlock much better interest rates, potentially saving you a significant amount of money over the years. You can easily check your score for free with services like Credit Karma or through your credit card provider. Generally, a score of 700 or higher is the sweet spot for getting the most competitive offers.

Once you have a handle on your credit situation, it’s time to start shopping around. This is a critical step—don’t just accept the first loan offer that comes your way. Taking the time to compare lenders is the key to finding the best possible terms.

You’ll find there are a few main places to look:

A smart strategy is to get pre-qualified with a few different lenders. This lets you see the actual rates and terms you could get without impacting your credit score, as it only requires a "soft" credit check.

Let's put this into a real-world context. Say you’re looking to finance a $15,000 procedure, like a tummy tuck, with a five-year (60-month) loan. The interest rate you end up with will dramatically change what you pay in the long run.

Here’s a quick breakdown to show you what I mean:

As the table shows, a better interest rate does more than just lower your monthly payment—it can save you thousands of dollars. This is exactly why comparing offers is an absolute must.

Also, keep a sharp eye out for any hidden costs like origination fees (a fee for processing the loan) or prepayment penalties. Always, always read the fine print before signing anything. The right loan should make your cosmetic journey easier, not add stress to it.

Aside from standard bank loans, you’ll find that many clinics have financing options built right into their practice, specifically for healthcare expenses. These tools, like medical credit cards and in-house payment plans, can make funding your procedure much more straightforward by keeping everything under one roof.

Medical credit cards are a common go-to. You’ve probably seen them offered for everything from dental work to vision care. They work just like a regular credit card but are dedicated solely to medical costs.

Their biggest draw is often a promotional 0% APR offer, which might last anywhere from six to 24 months. It’s a great feature that gives you a set amount of time to pay for your surgery without any interest piling up. Some third-party financing partners, like Cherry Payment Plans for medical procedures, offer a similarly structured way to spread out your payments.

That 0% interest period can be a lifesaver, but you have to read the fine print. Most of these cards operate on a system of deferred interest. This is a critical detail. It means that if you don't pay off every single penny of the balance before that promotional window closes, you’ll be hit with interest charges going all the way back to your original procedure date.

Let’s say you finance a $5,000 procedure on a 12-month, 0% plan. If you still have a $100 balance when that year is up, the interest isn't just calculated on the remaining hundred bucks. You could suddenly owe interest on the entire $5,000, calculated from day one. That’s a nasty surprise that can add hundreds, or even thousands, to your final cost.

Before you sign on the dotted line, always ask what the interest rate will be after the promotional period. More importantly, be realistic about your ability to pay off the full amount in time. A little convenience isn't worth a mountain of unexpected debt.

Another path worth serious consideration is setting up an in-house payment plan directly with our office. This route bypasses third-party lenders entirely, which almost always leads to a simpler and more personal experience. Since you’re working with a team you already know and trust, it just feels less daunting.

These plans are all about flexibility. Here at Cape Cod Plastic Surgery, we sit down with our patients to figure out a payment schedule that actually works for them. To see what that might look like for your procedure, you can find more information about our cosmetic surgery payment plans.

While credit cards are often used for smaller treatments, it’s a different story for larger surgeries. North America accounts for over 30% of the cosmetic surgery market, and while many people use credit, savvy patients often look for structured payment options to avoid those high interest rates. It really highlights why it’s so important to look at all your options before committing to one financing method.

While financing options make cosmetic procedures immediately accessible, there's a lot to be said for the tried-and-true method: saving. It's the most straightforward and, financially speaking, the savviest way to go.

When you pay with your own funds, the price you see is the price you pay. Period. No interest, no monthly payments, no debt. It's a path that offers total financial freedom and the peace of mind that comes with it.

Of course, this approach takes planning and a bit of discipline, but it’s more achievable than you might think. The best place to start is by opening a savings account dedicated solely to your procedure. I always recommend a high-yield savings account because it’ll earn more interest than a standard one, giving your funds a little boost while you save.

Once you have a dedicated account, it’s time to figure out how to fund it. This begins with a hard, honest look at your monthly budget.

Go through your spending line by line, especially the non-essentials. Think about how much you spend on dining out, subscription boxes you forget about, or that daily latte. You'd be amazed how quickly those small expenses add up and how much you can redirect toward your goal.

A couple of practical tips I’ve seen work wonders for my patients:

A clear savings plan turns a big, intimidating number into a series of small, manageable monthly steps. When you know exactly what you’re working toward and see real progress, the whole journey feels empowering.

Cutting back is one thing, but what about bringing more in? If you want to speed up your timeline, look for ways to boost your income, even temporarily.

Consider taking on some side hustle jobs like freelance writing or dog walking. You could also sell items you no longer use online or see if there are opportunities for extra hours at your current job. Every extra dollar gets you closer.

To make your plan truly effective, you need a clear target. Get a realistic idea of what your procedure might cost by checking out our guide on plastic surgery cost statistics and average prices. Once you have that concrete number, you can map out a timeline and celebrate every milestone you hit along the way.

Alright, you've explored the different avenues for financing your procedure. Now it's time to get everything in order and make a final, confident decision. This is your pre-op checklist for the financial side of things—getting it right now makes everything that follows so much smoother.

If you're leaning towards a loan or a medical credit card, any lender will need to see some basic paperwork. They're essentially verifying your identity and making sure you have the income to comfortably manage the payments. Getting these documents ready before you even apply is a smart move.

Before you start filling out forms, do yourself a favor and get a little file together. It's a simple step that can shave days off the approval process.

You'll almost certainly need:

Having this ready to go shows lenders you're organized and serious, which never hurts.

I've seen it happen before: a patient focuses only on the surgeon's fee and gets caught off guard by the other costs. The quote you receive is just one part of the total investment. To make sure you’re borrowing the right amount, you need to see the entire financial picture.

A detailed cost breakdown is non-negotiable. Your quote should clearly itemize every single charge so there are no surprises down the line. This transparency is a hallmark of a trustworthy practice and the foundation of a sound financial plan.

Make sure the total amount you finance accounts for everything:

Knowing the true all-in cost from the outset means you can secure one financing plan that covers it all. No last-minute stress.

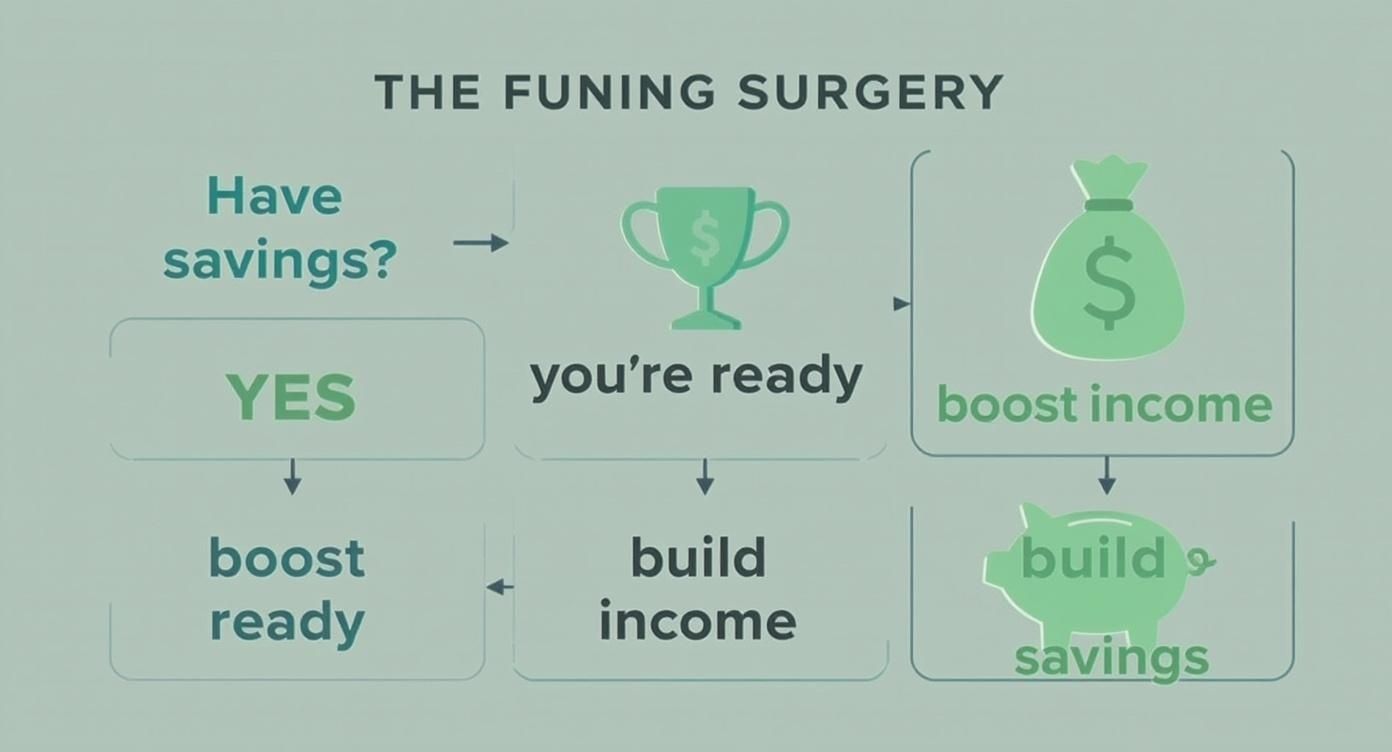

This decision tree gives you a great visual for mapping out your best path forward.

As you can see, having savings is the most straightforward route. If that's not your situation, the focus shifts to actionable steps like building a dedicated savings fund or exploring the best lending options available to you.

Once you have a few pre-approved offers in hand, resist the temptation to just pick the one with the lowest monthly payment. You need to dig a little deeper to see which one offers the best value over the long haul.

I suggest creating a simple chart or spreadsheet to compare them side-by-side. Focus on these three key factors for each loan or card offer:

Making a smart financing choice is the final piece of the puzzle. By preparing your documents, understanding the full cost, and carefully comparing your offers, you can proceed with absolute confidence. You’ll know you've made a decision that honors both your aesthetic goals and your financial well-being.

Thinking about the financial side of cosmetic surgery naturally brings up a lot of questions. Even after you've looked at the different ways to pay, a few uncertainties might still be nagging you. My goal here is to give you clear, straightforward answers to the questions I hear most often, so you can feel confident moving forward.

Yes, it's absolutely possible, though I'll be honest—your options will be a bit more limited. There are lenders out there who specialize in working with lower credit scores, but they usually balance out their risk by charging higher interest rates. It's a classic trade-off: you get the accessibility, but it costs more over time.

Another path to consider is a secured loan, where you'd use an asset like your car as collateral. We also work with patients on in-house payment plans, which often have more forgiving approval requirements than a big bank would. The most important thing is to be open about your situation when we talk. That way, we can look at every single path available to you.

Your credit score is just a snapshot in time, not a permanent roadblock. I've seen many patients take a few months to boost their score before applying for financing. This simple step often gets them much better rates and saves them a ton of money in the long run.

This is probably the number one question I get, and the short answer is usually no—but there are some very important exceptions. Health insurance plans just don't cover procedures that are done for purely cosmetic reasons.

However, if a procedure is deemed medically necessary, you might get partial or even full coverage. A perfect example is a rhinoplasty to fix a deviated septum that's causing real breathing problems. Another common one is breast reconstruction after a mastectomy. The key is getting proper documentation from your primary doctor and then talking directly with your insurance provider to find out exactly what your policy covers.

While both get the job done, they're built differently. A personal loan is pretty straightforward: a bank, credit union, or online lender gives you a lump sum of cash you can use for anything. The flexibility is great.

A medical loan, on the other hand, is designed specifically for healthcare costs. These are often available through companies that partner directly with our practice. The big advantage here is that they can sometimes come with promotional 0% interest periods, a lot like medical credit cards. The only catch is the funds can only be used to pay for your procedure.

Figuring this out really comes down to two things: the total cost of your procedure and how disciplined you are with your finances.

A credit card can be a fantastic tool for smaller, non-invasive treatments. This is especially true if you have a card with a 0% introductory APR. It’s like a short-term, interest-free loan, as long as you pay off the full balance before that promotional period ends.

For bigger surgeries with higher price tags, a personal loan is almost always the smarter way to go. You get a structured repayment plan with a fixed interest rate, which is typically much lower than the standard rate on a credit card. That predictability makes budgeting a whole lot easier and can save you a substantial amount of money on interest over the life of the loan.

For more general information, you might find our list of frequently asked questions about cosmetic surgery procedures helpful as you continue your research.

Ready to take the next step in your aesthetic journey? At Cape Cod Plastic Surgery, we're here to help you navigate your financing options and create a plan that aligns with your goals. Schedule your consultation with Dr. Fater today by visiting us at https://ccplasticsurgery.com.

Our 2026 guide explains precisely how does botox work. Discover its science, procedure, benefits, and risks in simple terms to see if it's for you.

July 7, 2026

Your Guide to Breast Implant Choices: Saline, Silicone, and Gummy Bear

July 6, 2026

Fat Transfer vs Filler: Our expert 2026 guide compares longevity, cost, recovery, and safety to help you choose your best option.

Cape Cod Plastic Surgery offers expert cosmetic and reconstructive procedures in a safe, accredited setting. Led by Dr. Marc Fater, we combine advanced techniques with personalized care to help you look and feel your best.

Monday: 9:00 AM – 5:00 PM

Tuesday: 9:00 AM – 5:00 PM

Wednesday: 9:00 AM – 5:00 PM

Thursday: 9:00 AM – 5:00 PM

Friday: 9:00 AM – 5:00 PM